Image gathered from here

Overall, I thought this was a pretty good read. The author primarily focuses on how Millennials need to take advantage of our most valuable asset, time. For a lot of us, we have 40 some years until we plan on retiring. This provides a significant amount of time for our net worth to grow.

The author discusses how the Great Recession has shaped Millennials into one of the most financially conservative generations ever. One statistic used that Millennials keep half of their assets in cash.

To combat this, the author gives a wide variety of reasons why people need to look into stocks, primarily through a specific screening that is influenced by cheap, worldly stocks. The main medium to do this is through the right mutual fund.

One thing that I pulled from the book was that over a long period of time stocks pose very minimal risk and that bonds do not present a viable option for growth in this day and age. Another aspect from this book that I found was that there is more risk in not investing than investing.

O'Shaughnessy poses some very realistic risks for not investing. In order to combat aging Baby Boomers, the United States will most likely be forced to raise taxes. The people mainly affected by these tax increases are people in prime income potential times in their career. To avoid this, Millennials need to divert resources into earning a good base. This way our money has time to compound over time.

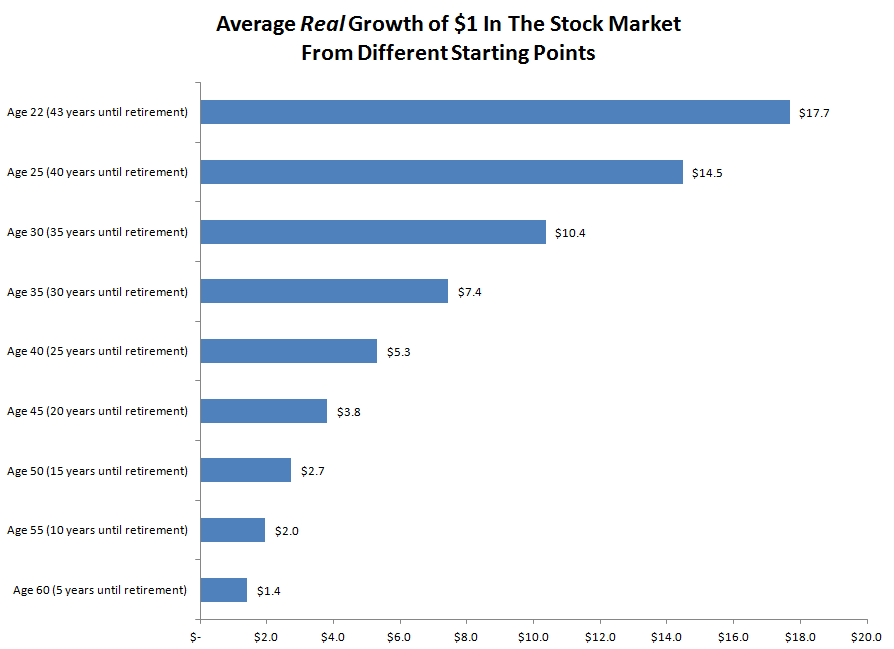

One last point that I want to make about this book is that the author stresses that Millennials need to understand that we will most likely not have Social Security or a pension to help fund our retirement. This has the potential to be a very large crisis for our generation in the future if people do not take the necessary steps. For me, I knew that I needed to start to invest when I saw this figure.

Image sourced from here

To put it in perspective, if you maxed out your 401(k) at $17,500 at age 15, the contribution would be worth $253,750! At age 40, this number drops to $92,750. This is a huge difference!

Take the time to invest and check out this book.

Author: Patrick O'Shaughnessy

Website: www.millennialinvest.com/

Twitter: @millennial_inv